With the aim of transforming the European Union (EU) into a “modern, resource-efficient and competitive economy,” the European Commission (EC) passed the European Green Deal in 2020. This brought the EC one step closer to directing capital toward projects and investments that would contribute to sustainable growth. To provide a common language and a clear definition of “sustainable,” the EC implemented the Taxonomy in 2020.

The EU Taxonomy is a classification system that defines criteria for economic activities intended to keep companies and societies aligned with the goal of achieving climate neutrality by 2050. This classification system aims to create security for investors; prevent greenwashing; accelerate companies’ progress toward becoming more climate friendly; mitigate market fragmentation; and help shift investments.

The EU Taxonomy in the Context of the Sustainable Finance Framework

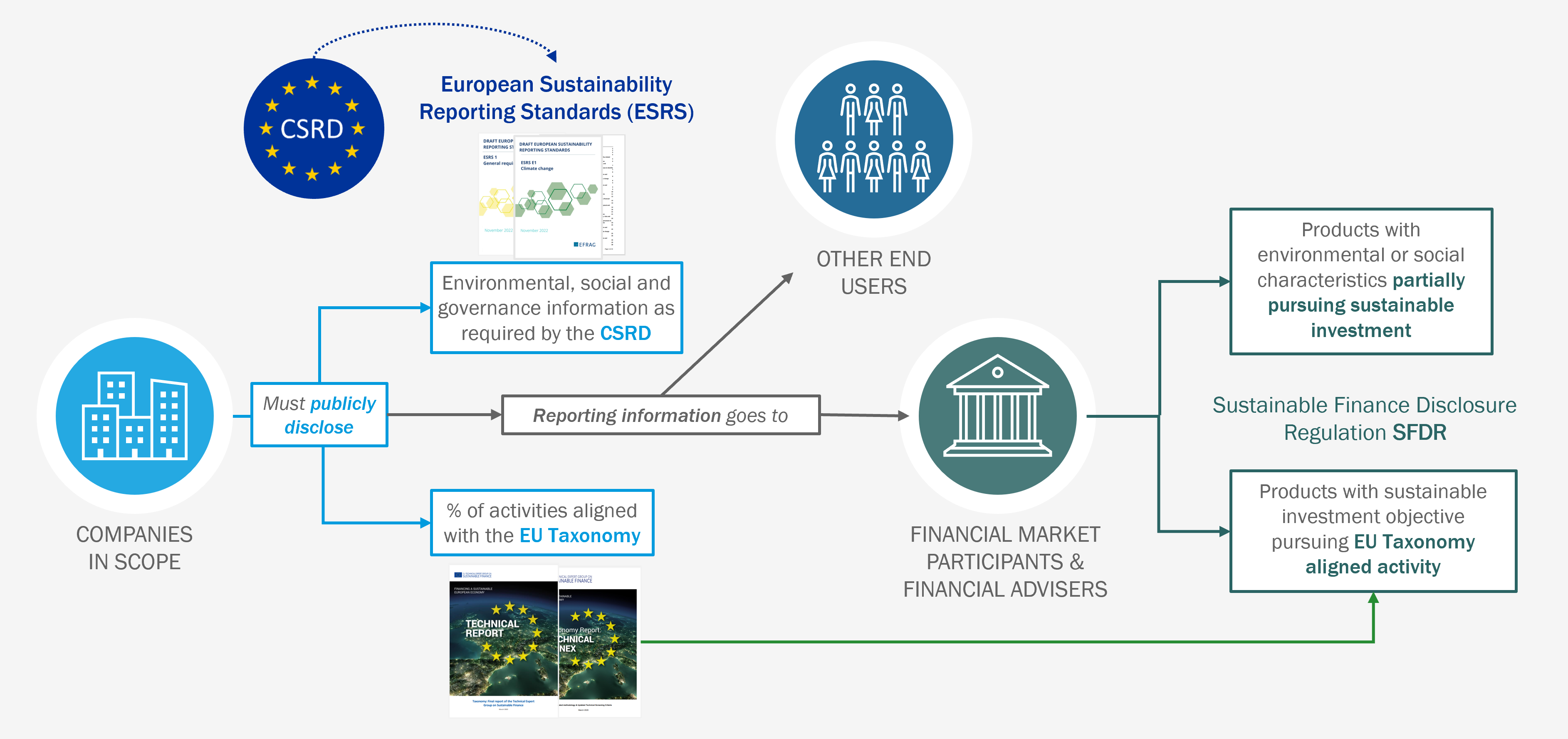

Together with the disclosure regimes of the Corporate Sustainability Reporting Directive (CSRD) and the Sustainable Finance Disclosure Regulation (SFDR), the EU Taxonomy forms the foundation of the EU sustainable finance framework.

How the EU Taxonomy Relates to Other EU Regulations

Source: Sphera, based on EC’s Sustainable Finance Taxonomy Factsheet

Companies that must report on sustainability topics have to include in their CSRD reports certain metrics based on the EU Taxonomy. Financial market players covered by the SFDR, in turn, also need the EU Taxonomy information from the companies’ CSRD reports for their disclosure requirements.

What Are the Disclosure Obligations of the EU Taxonomy Under the CSRD?

Companies that fall under the CSRD must disclose information related to their organization’s environmentally sustainable activities. Specifically, the CSRD requires companies to disclose in their annual reports the extent to which their activities are covered by and comply with the EU Taxonomy and its delegated acts.

From the reporting year 2022 onward, companies within the scope of the Non-Financial Reporting Directive (NFRD) must disclose their Taxonomy alignment on total capital expenditures (CapEx), operating expenditures (OpEx) and turnover. Starting in 2024, the CSRD replaces the NFDR.

EU Taxonomy Alignment: How It Works

The first step in EU Taxonomy alignment is to determine whether an economic activity is eligible; this means whether it is in scope of the Taxonomy or not. To pass the threshold for classification as sustainable, an eligible activity must meet the Technical Screening Criteria (TSC) set forth in the delegated acts.

Then, to be aligned with the Taxonomy, a sustainable economic activity must meet several criteria. First, it must make a substantial contribution to at least one of the Taxonomy’s six environmental objectives (described below). Additionally, the activity must “do no significant harm” to any other objectives, and it must comply with minimum safeguards.

EU Taxonomy: from Eligible to Aligned

Source: Sphera, based on https://ec.europa.eu/sustainable-finance-taxonomy/home

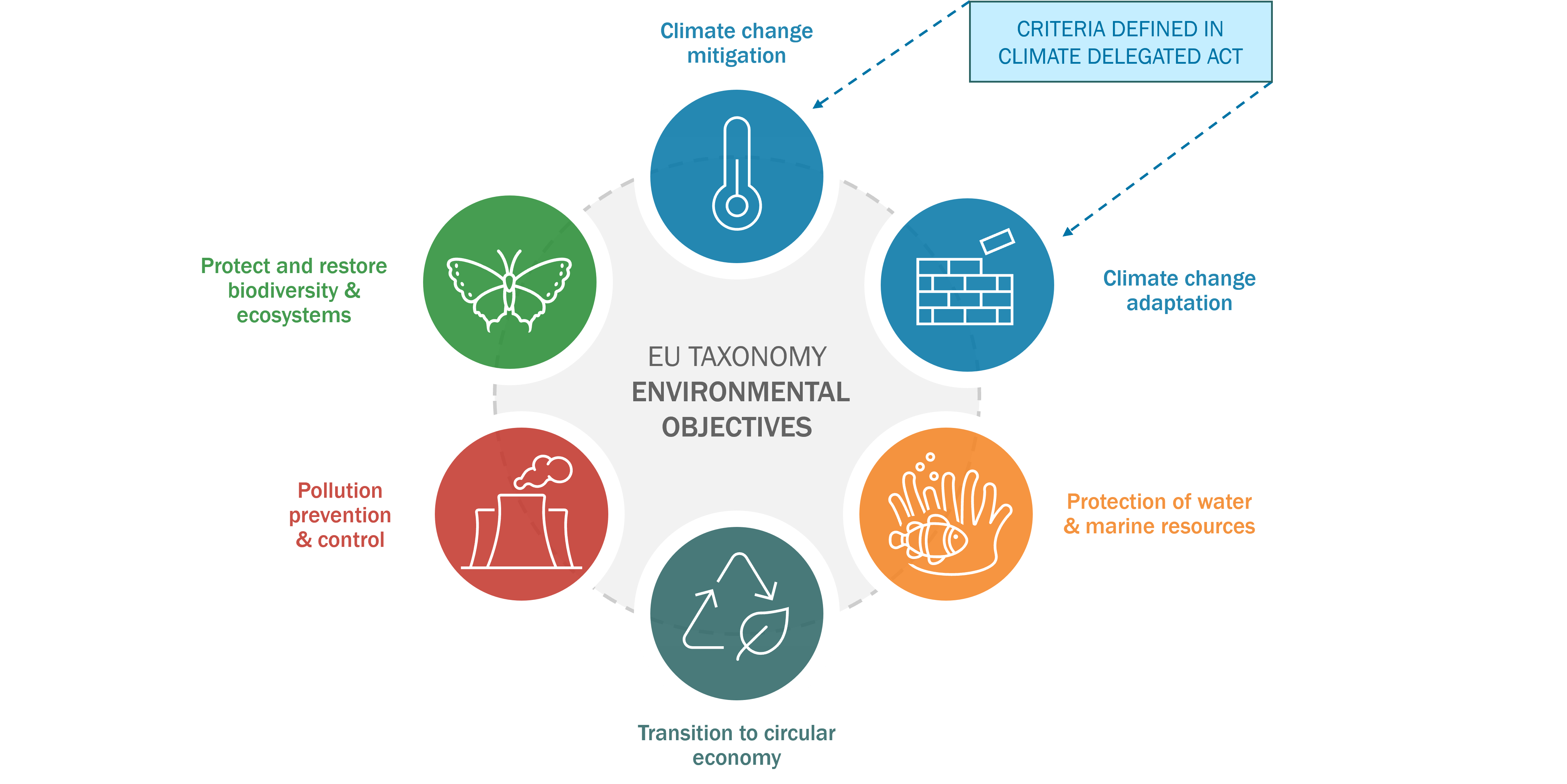

The six environmental objectives of the EU Taxonomy and a summary of their requirements as set out in the delegated acts are:

- Climate change mitigation: Activities qualifying for this objective focus on holding the increase in the global average temperature to well below 2°C. This objective also includes the pursuit of efforts to limit the increase to 1.5°C above pre-industrial levels.

- Climate change adaptation: This objective involves the process of adjusting to actual and expected climate change and its impacts. To qualify, an activity must substantially reduce the climate-related risk on that activity or on people, nature or assets.

- Protection of water and marine resources: The marine environment should be protected, preserved and restored. This objective encourages sustainable water use and activities that maintain biodiversity and provide dynamic, clean, healthy and productive oceans and seas.

- Transition to a circular economy: To qualify, activities must help maintain the value and efficient use of resources through waste prevention, re-use and recycling. The goal is to minimize waste and the release of hazardous substances at all stages of the product life cycle, including disposal.

- Pollution prevention and control: Activities in this category should prevent or reduce pollutants in the air, water or land (not including greenhouse gases) or improve air, water or soil quality while avoiding adverse impacts on human health and the environment.

- Protection and restoration of biodiversity and ecosystems: Economic activities must protect, conserve or restore biodiversity among terrestrial, marine and aquatic organisms and their ecosystems. Agricultural practices, land use and forest management must be sustainable.

EU Taxonomy: Environmental Objectives

Source: Sphera, based on https://ec.europa.eu/sustainable-finance-taxonomy/home

How to Prepare for EU Taxonomy Alignment

To disclose their Taxonomy alignment, companies must first create awareness of the EU Taxonomy requirements and their interrelation with other reporting practices such as the CSRD. Initial steps might include:

- Review and assessment of existing EU Taxonomy efforts and an initial data availability check for the required disclosure.

- Benchmarking and development of best practice, including insights on the challenges of applying the EU Taxonomy.

- Review of status and recommendation for EU Taxonomy disclosure in the context of the CSRD.

In addition, companies need to understand how and what to disclose, how to identify eligible activities and how to quantify the share of Taxonomy-eligible and non-eligible activities in CapEx, OpEx and turnover. Organizations will also need to test the eligible activities for their alignment with the Taxonomy criteria. This means a company could report their activities using the following sections: non-eligible activities; eligible but not yet aligned activities; and eligible activities that are aligned, along with the respective shares of CapEx, OpEx and turnover in each section.

How Sphera Can Help

Our experienced ESG consultants can help you prepare for EU Taxonomy alignment. This includes integrating EU Taxonomy reporting into existing processes and aligning with CSRD reporting. Sphera’s sustainability experts help you address the challenges of EU Taxonomy implementation. In doing so, Sphera’s consultants strive to deliver tailored approaches that consider relevant regulatory developments and updates impacting your business. Our modular project components can be customized to meet your specific needs and maturity level.