Under the Carbon Border Adjustment Mechanism (CBAM), manufacturers and importers must report on the embedded GHG emissions of carbon-intensive goods in six defined categories that enter the EU. As the transitional phase began in October 2023 and continues through December 2025, companies have little time to lose.

WHAT YOU NEED TO KNOW

The background and basics of the EU CBAM

Developed by the European Union, the CBAM is a carbon-pricing tool that aims to equalize carbon pricing on domestic and imported goods. The regulation aims to put a fair price on the carbon emitted from emission-intensive goods produced or sold in the EU.

To prevent “carbon leakage,” when companies move production out of the EU or procure from countries with less stringent carbon-pricing schemes, the CBAM obligations fall to importers. The regulation is intended to complement and reinforce the EU Emissions Trading System (ETS), a “cap and trade” system for reducing GHG emissions.

In short, the ETS caps emissions that companies may produce, but allows them to buy additional emissions from companies that do not use up their allowance. Although both the ETS and the CBAM put a price on carbon, the ETS applies primarily to intra-EU goods, while the CBAM covers goods imported from non-EU countries (except Iceland, Norway, Liechtenstein and Switzerland), mainly to address carbon leakage.

Also, identifying direct and indirect GHG emissions is key to the CBAM. Embedded emissions are those associated with materials, fuel carriers and processes that emit CO2 into the atmosphere. The emissions from all production activities are categorized as direct emissions. Those associated with precursors and contributors to manufacturing, such as the electricity generated for processes, are indirect emissions.

WHO THIS AFFECTS

Scope and reach of the CBAM

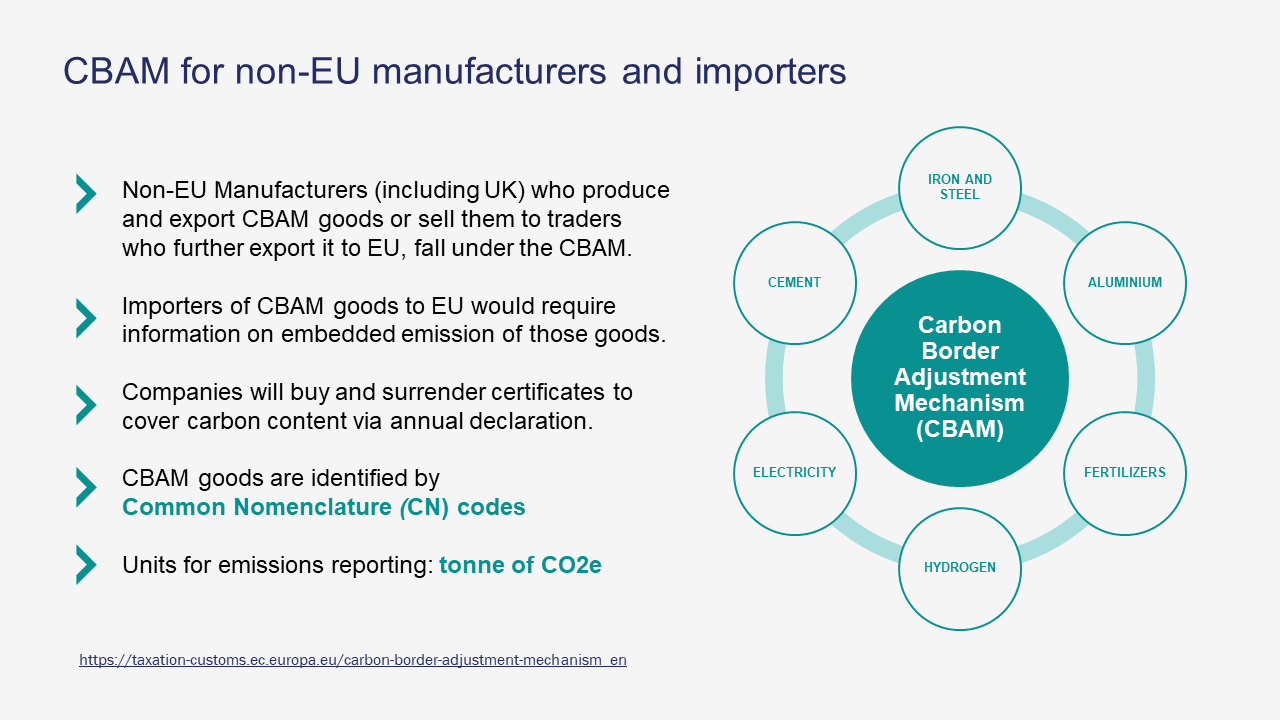

The CBAM regulation covers iron and steel, aluminum, fertilizers, cement, electricity and hydrogen from non-EU manufacturers, including the U.K. These six energy-intensive sectors potentially present a greater risk of carbon leakage.

Importers into the EU market must report the embedded GHG emissions of CBAM products, which are identified by eight-digit Common Nomenclature (CN) codes. The emissions calculations encompass processes such as manufacturing and the production of precursors, which are processes or materials used to produce complex goods. In steel production, for example, sinter, direct reduced iron (DRI) and ferromanganese (FeMn) are precursors.

With binding carbon reduction goals set by the Paris Agreement for worldwide climate neutrality by 2050, CBAM principles and calculations are increasingly attractive for other markets. For example, CBAM proposals are also under consideration in the United States.

WHAT YOU NEED TO DO

Five steps to prepare for the CBAM

Although manufacturers are responsible for compiling the data, importers face CBAM regulatory obligations. For each sector, the EU clearly defines boundaries and emissions that fall under the regulation.

For non-EU manufacturers, preparing for CBAM reporting involves these steps:

1. Define the system boundaries associated with the production processes. Identify the system boundaries, such as unit processes, inputs, outputs and impacts, for products intended for the EU. These boundaries essentially mirror those in the EU ETS and follow the same calculation methodology.

2. Identify relevant parameters and methods, then carry out monitoring. Parameters such as resources and fuel carriers emit direct GHG emissions, whereas electricity produced or consumed contributes to indirect GHG emissions. Precursor consumption also contributes to GHG emissions. The most commonly applied methodologies are calculation-based and measurement-based approaches.

3. Attribute emissions to production processes and to goods. Determine and categorize production and materials emissions, such as carbon in, carbon out, fuel coming in and process emissions. Include electricity and heat when these are sourced externally.

4. Add the specific embedded emissions of relevant precursors. Once the GHG emissions for the precursors are attributed, calculate the direct and indirect absolute embedded GHG emissions. For the CBAM, specific embedded GHG emissions are expressed per metric ton (tonne) of the imported goods.

5. Determine the specific embedded emissions of CBAM goods (CN code). Finally, include details such as the production facility and product specifications, then attribute the calculations of specific embedded, direct, indirect and total unit emissions to the products according to their CN codes.

For importers of carbon-intensive goods into the EU, complying with the CBAM involves the following:

1. Define the scope of goods concerned. Establish which goods will be included in the reporting and identify their CN codes from existing customs information. The CN codes can also be found in the annex of EU documentation. Alternatively, the manufacturer’s compliance department may have the information from other declarations.

2. Determine the reporting period to use. During the transitional phase, importers must submit a CBAM report on a quarterly basis for the previous quarter.

3. Identify and collect all the parameters needed to report. Identify the data that the manufacturer must provide for each product in terms of direct and indirect specific GHG embedded emissions.

4. Collect information on the carbon pricing jurisdiction. Find out whether a carbon pricing scheme exists in the products’ country of origin. Determine whether this scheme extends to the precursors.

5. Compile and declare to the CBAM Transitional Registry. The importer, also known as reporting declarant, must file the embedded GHG emissions report in the CBAM Transitional Registry. For access, importers need to be authorized by the National Competent Authority (NCA) of their member state.

FOR MORE CONTEXT

Comparing CBAM with carbon footprint calculations

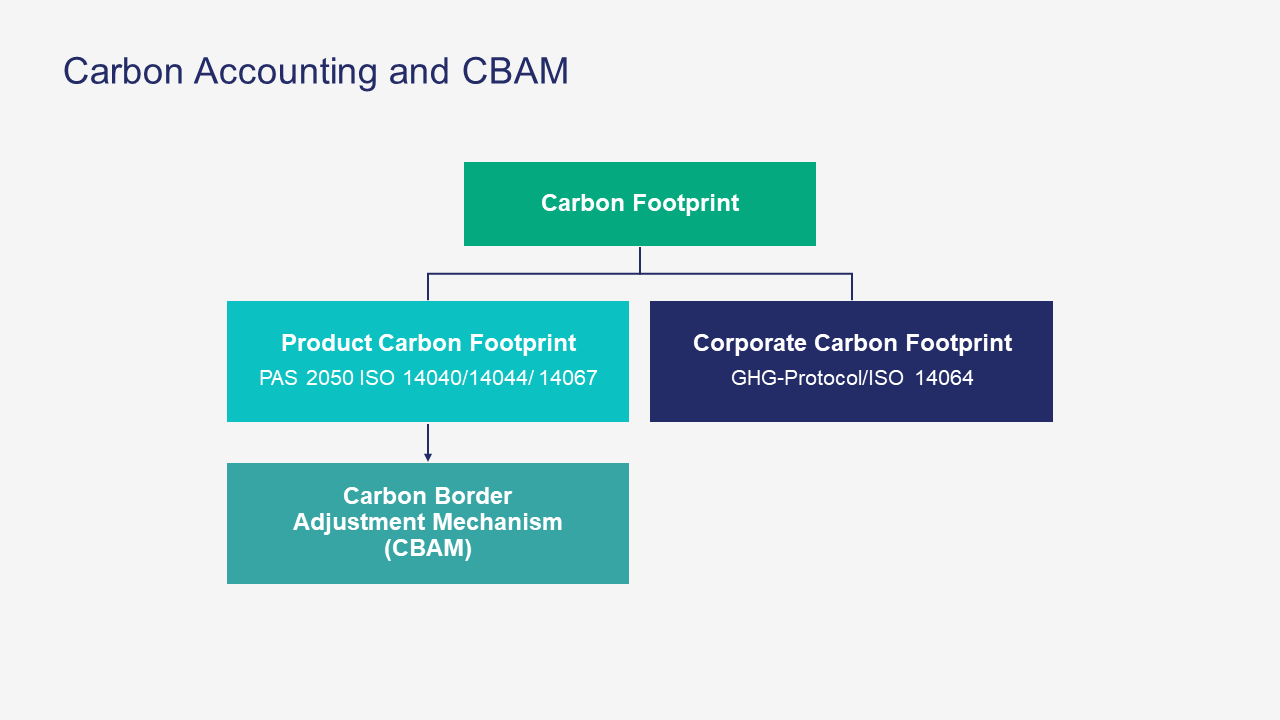

For more context, it is useful to understand how carbon accounting relates to the CBAM. A product carbon footprint (PCF) accounts for all greenhouse gas emissions attributable to the product along its life cycle.

The CBAM calculation is a part of the PCF, but has a narrower scope. If companies perform a life cycle assessment (LCA) or an environmental product declaration (EPD), this carbon footprint calculation is not sufficient for registration under the CBAM; but parts of it can be used, as defined in the EU calculation methodology.

For an EPD or an LCA, the upstream, production, usage and the end-of-life stages of a product are considered. The CBAM, on the other hand, only includes the GHG emissions from the relevant precursors and from the production process.

To support companies as they adjust to determining embedded GHG emissions, the EU has provided a list of global default values, which may be used through the first half of 2024. However, starting in the third quarter, companies are only allowed to use default values for 20% of the emissions total and only for complex goods. Any other values should be actual production data.

WHAT HAPPENS NEXT

Timeline for CBAM implementation

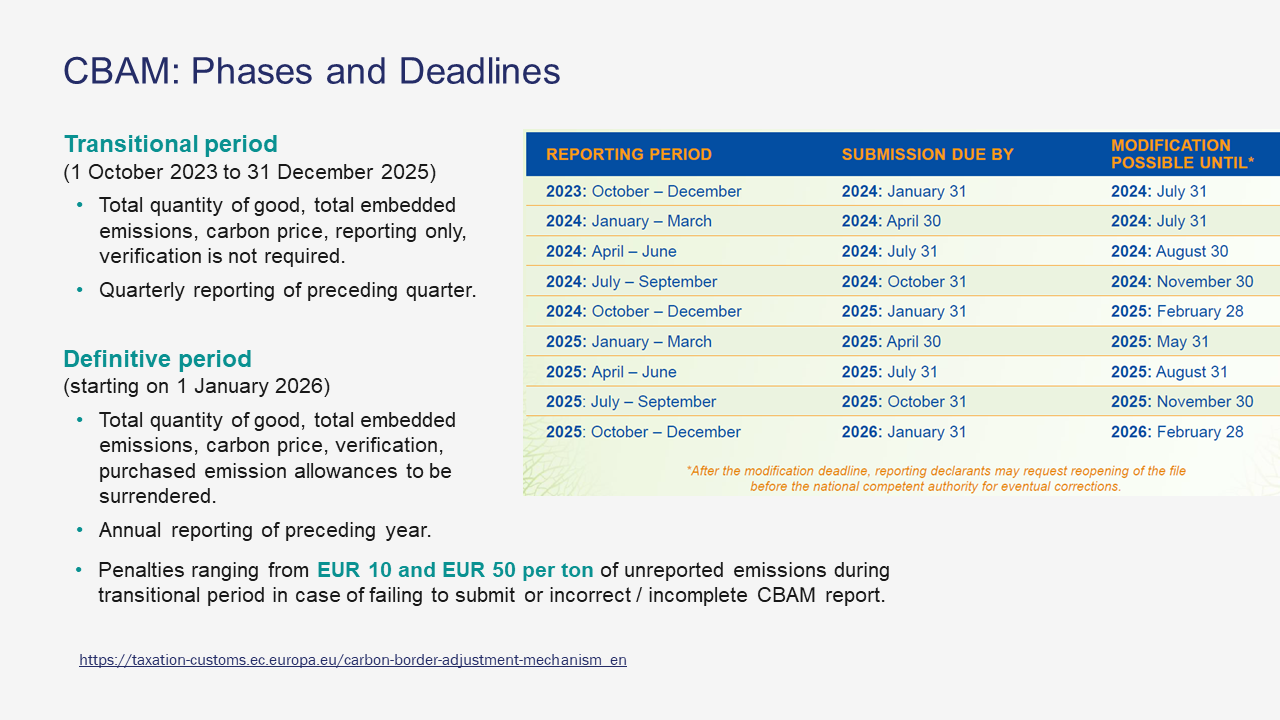

The CBAM transitional phase began in October 2023 and continues through December 2025. Currently, importers in the six sectors need to report the total embedded emissions on a quarterly basis, but verification is not required. Some allowances are available under the EU ETS.

When the transitional phase ends, verification will be mandatory and allowances may no longer be purchased. Importers must then submit reporting annually for the preceding year. If they fail to report, or unreported emissions are identified, they may have to pay penalties of €10 to €50 per ton of CO2 equivalent. The amount depends on whether the declarant needs to submit or complete the CBAM report and whether they implement the corrections specified by authorities.

Beginning with the permanent phase in 2026, companies will have to buy CBAM certificates to cover the carbon content of imports as declared in an annual report. The price is linked to the EU ETS allowances. Importers will then surrender the corresponding number of certificates for the year.

HOW SPHERA CAN HELP

Expert support for CBAM and carbon-related reporting

Sphera’s sustainability consultants can assist importers and manufacturers with carbon accounting, LCAs and product carbon footprint calculations. Our CBAM reporting template helps companies assess their specific embedded emissions. We support companies with:

Carbon emissions accounting. We offer workshops and support companies with calculations, reporting, declarations and quarterly update processes from the importer and exporter perspectives. We also facilitate carbon emissions accounting for installations or facilities.

LCA and product carbon footprint. With our background and expertise in LCA across numerous industries, we understand the process models, consumption of resources, fuel carriers, related process emissions and the emission factors. For CBAM, we help companies understand which CN codes apply and how to determine their products’ manufacturing and precursors’ GHG emissions.

Screening products for CBAM applicability. We explain how the CBAM template is generated and how to identify system boundaries and precursors. We guide customers in selecting a monitoring methodology; collecting and validating data; and calculating direct and indirect GHG emissions.

Data collection, validation and CBAM reporting. Sphera’s sustainability experts can build company-and product-specific GHG emissions calculators as per the CBAM requirement. Additionally, SpheraCloud Corporate Sustainability and Supply Chain Sustainability Software solutions enable the collection of sustainability data in the supply chain, which can be used to populate CBAM templates.

Put simply, the CBAM is about transparency. Accounting for the GHG emissions released by materials and during processes used in carbon-intensive sectors is the foundation. This involves collecting accurate and comprehensive product-specific data, including precursors. Reporting on domestic and imported goods ensures fair carbon pricing for all. Reducing GHG embedded emissions, not only in EU products, can help the global community meet climate-neutrality goals.

The information provided in this blog is for general information purposes only, may not be updated in real time and does not constitute legal advice. Please consult with your legal and other advisors to discuss your particular needs and circumstances.

Solutions in this article

Latest insights from Sphera

EU Battery Regulation carbon footprint requirements: How companies can prepare

EU Battery Regulation carbon footprint requirements: How companies can prepare

Simplification with substance: Why the ESRS Reset is a strategic opportunity

Simplification with substance: Why the ESRS Reset is a strategic opportunity

KAEFER strengthens global ESG reporting consistency with Sphera, improving audit readiness and sustainable decision-making