The Greenhouse Gas (GHG) Protocol categorizes greenhouse gas emissions into three groups or ‘Scopes’.

Scope 1 covers direct emissions from owned or controlled sources, while scope 2 includes indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the reporting company. Scope 3 includes all other indirect emissions from a company’s value chain.

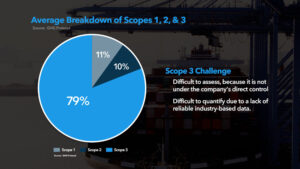

As they are traditionally the focus of corporate reporting, Scope 1 and Scope 2 have a mature data foundation for their measurement and assessment. The quantification, reduction and reporting of Scope 3 emissions, on the other hand, is fraught with more difficulties.

What Are Scope 3 Emissions?

The GHG Protocol classifies Scope 3 emissions as all indirect emissions that result from assets not controlled or owned directly by the organization but occurs in its value chain. That is why it is often called value chain emissions, and its sources can include emissions both upstream and downstream activities of the organization.

The Corporate Value Chain (Scope 3) Accounting and Reporting Standard of the GHG Protocol groups Scope 3 emissions into 15 dedicated categories that include business activities common to many organizations. These categories give companies a framework to measure, manage, and reduce emissions in key areas across a corporate value chain.

Some of the Scope 3 categories (e.g., business travel and employee commuting) are easier to quantify than others (e.g., purchased goods and services, or use of sold products), and not all 15 categories are relevant for every company. Some examples of the most important upstream and downstream categories are:

- Purchased goods and services (focused on the upstream supply chain)

- Processing and use of sold products.

- Upstream and downstream transportation and distribution

- Waste generated in operations and end-of-life treatment of sold products.

Why Is Scope 3 Emissions Accounting Important?

Depending on the industry, the value chain emissions can comprise up to 80% of your company’s overall environmental impact. Therefore, they play an important role in a robust science-based decarbonization strategy toward net zero.

Since Scope 3 emissions are not directly under a company’s control, they are difficult to assess. But companies cannot afford to bypass or ignore them anymore. Scope 3 emissions have to be quantified based on reliable industry-based data and in the right way. Without a proper Scope 3 strategy, businesses could face reputational damage due to green-washing, high capital costs, financial risks, or even lose their “license to operate.”